Introduction: The return filing under Indian income tax has under gone sea

change after the introduction of efiling. The major problem faced by most of

the assessees, being a private trust, is how to file their tax return, inter

alia, the type of form and whether to efile or not. The authors have tried to

itemize the various ways to combat tricky situations while filing the tax

returns for private trust. The readers can go through the below given FAQs to

help themselves while filing the return for PRIVATE TRUSTS.

Article

Index:

1.

Types of private trusts for the purpose of return filing.

2.

Type of return for private trusts for efiling/manual filing

3.

Tax rate applicable for trusts mentioned above.

4.

Is PAN mandatory for private trusts? How to obtain PAN for private trust?

5.

How to calculate tax in the case of private specific trusts and whether more

than 1 return has to be filed, in the case of multiple beneficiaries, by the

trustee(s)?

6.

How to compute tax in case of private discretionary trust?

7.

Whether a private trust can accept gifts from related and unrelated persons and

whether trust property is taxable in the hands trustee as gift when the same is

transferred to the trust?

8.

Tax status-when a trust is revocable, irrevocable and revoked?

9.

Whether a settlor can transfer trust income, without transferring the trust

property?

10.

Tax treatment in the hands of settlor-when property is transferred by him to

the trust?

11.

Minor and private trust-tax consequences?

12.

Spouse and private trust-tax consequences?

13.

Daughter-in-law and private trust-tax consequences?

14.

Is private trust a real tax planning tool? MUST

READ

15.

Whether private trust can claim deductions u/c VIA?

16.

More FAQs?

1. Types of private trusts for the purpose of return filing.

{kind=link}

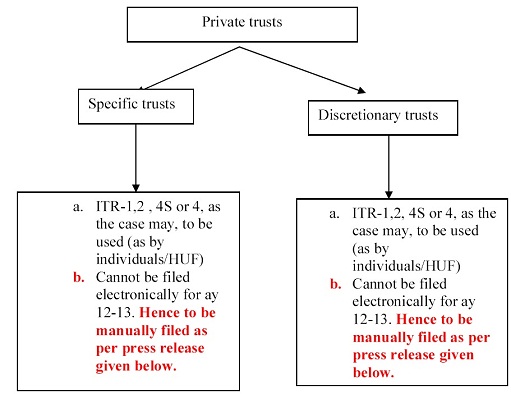

2.

Type of return for private trusts for efiling/manual filing-for AY 2012-13.

{kind=link}

Imp.

Note: for income tax purposes a private trust is treated as individual.

|

Sl. No

|

Form no.

|

conditions

|

|

1.

|

ITR no. 1-sahaj

|

This return form is to be used by

the Individual whose total income for the Assessment Year 2012-13 includes1.

Income from salary/pension :or2. Income from one house property(excluding

where loss brought forward from previous year):or3. Income from other sources(

excluding winnings from lottery and income from races horses)

|

|

2.

|

ITR 2-not for business and

profession income

|

This Return Form is to be used by

an individual or an Hindu Undivided Family whose total income for the

assessment year 2012-13 includes:-(a) Income from Salary /Pension ; or(b)

Income from House Property; or(c) Income from Capital Gains; or(c) Income from

Other Sources (including Winning from Lottery and Income from Race Horses).

|

|

3.

|

ITR – 4

|

For individuals and HUFs having

income from a proprietary business or profession and income under other heads

|

Press

note/release

Rule

12 of the Income-tax Rules, 1962 mandates that an individual or Hindu undivided

family, if his or its total income or the total income in respect of which he

is or it is assessable under theAct, during the previous year, exceeds ten lakh

rupees, shall furnish the return electronically for the assessment year 2012-13

and subsequent assessment years.

It

has been brought to the notice of the Board that the s in agents of

non-residents, within the meaning of section 160(1) (i) of the Income –tax Act,

are facing difficulties in electronically furnishing the returns of

non-residents. This is because there may be more than one agent of the

non-resident in India for different transactions or a person in India may be an

agent of more than one non-resident. Such situations are not covered by the

existing e-filing software which functions on the principle of one assessee-one

PAN-one return.

It

has also been brought to the notice of the Board that ‘private discretionary

trusts’ having total income exceeding ten lakh rupees are facing problems in

filing their return of income electronically in cases where they are filing

their return in the status of an individual. This is because status of a

private discretionary trust has been held in law as that of an ‘individual’.

The existing e-filing software does not accept the return of a private

discretionary trust in the status of an ‘individual’.

Accordingly

it has been decided by the Board that:

(i)

it will not be mandatory for agents of non-residents, within the meaning of

section 160(1) (i) of the Income –tax Act, if his or its total income exceeds

ten lakh rupees, to electronically furnish the return of income of

non-residents for assessment year 2012-13;

(ii)

it will not be mandatory for ‘private discretionary trusts’, if its total

income exceeds ten lakh rupees, to electronically furnish the return of income

for assessment year 2012-13.

DSM/SS/Hb

(Release ID :85615)

Note:

in our opinion, the intent of the department is to exclude private trusts of

both types from efiling be it discretionary or specific trust for the ay 12-13

3. Tax rate applicable for trusts

mentioned above.

See

the diagram below for better understanding:

{kind=link}

Notes:

Point

1: in the following case rates

applicable to Individuals will be charged:

- If the trust has been declared

by way of a will from which business income is derived; and

- It is exclusively declared for

the benefit of any relative dependent on the settlor for support and

maintenance; and

- The trust is the only trust so

declared by the settlor.

Point

2: in the following cases rates

applicable to Individuals will be charged:

1.

Where none of the beneficiaries

- Has taxable income exceeding

180000.00/1,90,000/250000 for ay 12-13

- Is a beneficiary under any

other private trust; or

2.

Where the relevant income or part of the relevant income is receivable under a

trust declared by any person by will and such trust is the only trust so

declared by him; or

3.

Where the trust yielding the

relevant income or part thereof was created by a non-testamentary instrument

before 1-3- 1970 and the A.O. is satisfied that it was created bona fide for

the benefit of the dependant relatives of the settlor, or where the settlor is

HUF, exclusively for the benefit of the dependant members.

4.

Where the relevant income is

receivable by the trustees on behalf of a provident fund, superannuation fund,

gratuity fund or pension fund or any other fund created bona fide by a person

carrying on a business or professional exclusively for the benefits of his

employees.

Tax

treatment of settlor / grantor

- If the trust effectively

alienates income from the settlor/grantor, income tax liability thereon

shall stand transferred to the trustee(s).

- However, the settlor/grantor

continues to be liable to income tax on income from the settled property

to the extent that it is for the immediate or deferred benefit of a spouse

or minor child.

- Stamp duty is payable on the

transfer of immovable property.

4.

Is PAN mandatory for private trusts? How to obtain PAN for private trust.

Yes,

the private trust needs to apply for PAN in order to file the ITR. The PAN

application can be made to a specified authority along with the following

documents;

1. Address proof

2. Bank a/c of the private trust.

3. Trust deed

5.

How to calculate tax in the case of private specific trusts?

1. The tax in the case of private

specific trusts is to be calculated in the same way as calculated for

individuals slab rate starting from Rs. 1,80,000.00 (in our opinion the slab

should depend upon the beneficiaries status-if the trust has solo beneficiary)after

allowing all deductions and set-off of losses.

2. If there is more than one

beneficiary, then the slab should start from Rs.1 80,000.00.

3.

However, where the trust has business income, the rate applicable will 30%+3%,

however, if the following three conditions are met cumulatively, the tax rate

will be slab rate:

- If the trust has been declared

by way of a will from which business income is derived; and

- It is exclusively declared for

the benefit of any relative dependent on the settlor for support and

maintenance; and

- The trust is the only trust so

declared by the settlor.

4.

In case of more than one beneficiary, only one return will be filed by the

trustee(s) in the representative capacity.

6.

How to calculate tax in the case of private discretionary trusts?

a.

If income does not includes Profit & Gain From Business & profession

(PGBP) income-

i.

General rate-30%+3% (EC)

ii.

. Slab rate if the following conditions are satisfied:

- Where none of the beneficiaries

–

Has taxable income exceeding 180000.00/1,90,000/250000 for ay 12-13

–

Is a beneficiary under any other private trust; or

- Where the relevant income or

part of the relevant income is receivable under a trust declared by any

person by will and such trust is the only trust so declared by him; or

- Where the trust yielding the

relevant income or part thereof was created by a non-testamentary

instrument before 1-3-1970 and the A.O. is satisfied that it was created

bona fide for the benefit of the dependent relatives of the settlor, or

where the settlor is HUF, exclusively for the benefit of the dependent

members.

- Where the relevant income is

receivable by the trustees on behalf of a provident fund, superannuation

fund, gratuity fund or pension fund or any other fund created bona fide by

a person carrying on a business or professional exclusively for the

benefits of his employees.

b.

If income includes PGBP income-

i.

General rate-30%+3%

ii.

Slab rate if the following conditions are satisfied:

- If the trust has been declared

by way of a will from which business income is derived; and

- It is exclusively declared for

the benefit of any relative dependent on the settlor for support and

maintenance; and

- The trust is the only trust so

declared by the settlor.

iii. In case of more than one beneficiary, only one return will

be filed by the trustee in the representative capacity.

7.

Whether a private trust can accept gifts for related and unrelated persons and

whether trust property is taxable in the hands trustee as gift when the same is

transferred to the trust?

Generally

speaking a trust is created by a person the watch interests of his “relatives

“, hence in majority of cases the tax shall not be chargeable in case property

gifted/transferred, whether movable or immovable, as per section 56(2)(vi) and

56(2) (vii) in the hands of the transferee.

56

(2) [(vi)

[(vi)

where any sum of money, the aggregate value of which exceeds fifty thousand

rupees, is received without consideration, by an individual or a Hindu

undivided family, in any previous year from any person or persons on or after

the 1st day of April, 2006 [but before the 1st day of October, 2009], the whole

of the aggregate value of such sum:

Provided

that this clause shall not apply to

any sum of money received—

(a)

from any relative; or

(b)

on the occasion of the marriage of the individual; or

(c)

under a will or by way of inheritance; or

(d)

in contemplation of death of the payer; or

(e)

from any local authority as defined in the Explanation to clause (20) of

section 10; or

(f)

from any fund or foundation or university or other educational institution or

hospital or other medical institution or any trust or institution referred to

in clause (23C) of section 10; or

(g)

from any trust or institution registered under section 12AA.

Explanation.—For

the purposes of this clause, “relative” means—

(i)

spouse of the individual;

(ii)

brother or sister of the individual;

(iii)

brother or sister of the spouse of the individual;

(iv)

brother or sister of either of the parents of the individual;

(v)

any lineal ascendant or descendant of the individual;

(vi)

any lineal ascendant or descendant of the spouse of the individual;

(vii)

spouse of the person referred to in clauses (ii) to (vi);]

[(vii)

where an individual or a Hindu undivided family receives, in any previous year,

from any person or persons on or after the 1st day of October, 2009,—

(a)

any sum of money, without consideration, the aggregate value of which exceeds

fifty thousand rupees, the whole of the aggregate value of such sum;

[(b)

any immovable property, without consideration, the stamp duty value of which

exceeds fifty thousand rupees, the stamp duty value of such property;]

(c)

any property, other than immovable property,—

(i)

without consideration, the aggregate fair market value of which exceeds fifty

thousand rupees, the whole of the aggregate fair market value of such property;

(ii)

for a consideration which is less than the aggregate fair market value of the

property by an amount exceeding fifty thousand rupees, the aggregate fair

market value of such property as exceeds such consideration :

Provided

that where the stamp duty value of

immovable property as referred to in sub-clause (b) is disputed by the assessee

on grounds mentioned in sub-section (2) of section 50C, the Assessing Officer

may refer the valuation of such property to a Valuation Officer, and the

provisions of section 50C and sub-section (15) of section 155 shall, as far as

may be, apply in relation to the stamp duty value of such property for the

purpose of sub-clause (b) as they apply for valuation of capital asset under

those sections :

Provided

further that this clause shall not apply to

any sum of money or any property received—

(a)

from any relative; or

(b)

on the occasion of the marriage of the individual; or

(c)

under a will or by way of inheritance; or

(d)

in contemplation of death of the payer or donor, as the case may be; or

(e)

from any local authority as defined in the Explanation to clause (20) of

section 10; or

(f)

from any fund or foundation or university or other educational institution or

hospital or other medical institution or any trust or institution referred to

in clause (23C) of section 10; or

(g)

from any trust or institution registered under section 12AA.

Explanation.—For

the purposes of this clause,—

(a)

“assessable” shall have the meaning assigned to it in the Explanation 2 to

sub-section (2) of section 50C;

(b)

“fair market value” of a property, other than an immovable property, means the

value determined in accordance with the method as may be prescribed;

(c)

“jewellery” shall have the meaning assigned to it in the Explanation to

sub-clause (ii) of clause (14) of section 2;

(d)

“property” [means the following capital asset of the assessee, namely:—]

(i)

immovable property being land or building or both;

(ii)

shares and securities;

(iii)

jewellery;

(iv)

archaeological collections;

(v)

drawings;

(vi)

paintings;

(vii)

sculptures; [***]

(viii)

any work of art; 1[or]

[(ix)

bullion;]

[(e) “relative” means,—

(i)

in case of an individual—

(A)

spouse of the individual;

(B)

brother or sister of the individual;

(C)

brother or sister of the spouse of the individual;

(D)

brother or sister of either of the parents of the individual;

(E)

any lineal ascendant or descendant of the individual;

(F)

any lineal ascendant or descendant of the spouse of the individual;

(G)

spouse of the person referred to in items (B) to (F); and

(ii)

in case of a Hindu undivided family, any member thereof;]

(f)

“stamp duty value” means the value adopted or assessed or assessable by any

authority of the Central Government or a State Government for the purpose of

payment of stamp duty in respect of an immovable property;]

8.

Tax status-when a trust is revocable,irrevocable and revoked.

|

Sl.No.

|

Particulars

|

Consequences

|

|

1

|

Where the trust is revocable from

the beginning.

|

The income from trust income will

be taxable in the hands of the settlor from inception section 61

|

|

2.

|

When the trust is irrevocable for

a specified period under section 62

|

During the period the trust was

not revocable, the trustee shall be liable to pay tax in representative

capacity.

|

|

3.

|

When the trust, which was

irrevocable gets revoked due to death of the beneficiary(ies)

|

The property will get back to the

settlor or any other person specified in the trust deed or the legal

inheritor of the property and he shall be liable to pay tax on the income

from such property from the date of transfer.

|

61- REVOCABLE TRANSFER OF ASSETS.

All income arising to any person by

virtue of a revocable transfer of assets shall be chargeable to income-tax as

the income of the transferor and shall be included in his total income.

62-

TRANSFER IRREVOCABLE FOR A SPECIFIED PERIOD.

(1)

The provisions of section 61 shall not apply to any income arising to any

person by virtue of a transfer –

(i)

By way of trust which is not revocable during the lifetime of the beneficiary,

and, in the case of any other transfer, which is not revocable during the life

time of the transferee; or

(ii)

Made before the day of April, 1961, which is not revocable for a period

exceeding six years :

Provided

that the transferor derives no direct or indirect benefit from such income in

either case.

(2)

Notwithstanding anything contained in sub-section (1), all income arising to

any person by virtue of any such transfer shall be chargeable to income-tax as

the income of the transferor as and when the power to revoke the transfer

arises, and shall then be included in his total income.

Section

63- “TRANSFER” AND “REVOCABLE TRANSFER” DEFINED.

For

the purposes of sections 60, 61 and 62 and of this section, –

(a)

A transfer shall be deemed to be revocable if –

(i)

It contains any provision for the re-transfer directly or indirectly of the

whole or any part of the income or assets to the transferor, or

(ii)

It, in any way, gives the transferor a right to re-assume power directly or

indirectly over the whole or any part of the income or assets;

(b)

“Transfer” includes any settlement, trust, covenant, agreement or arrangement

9.

Whether a settlor can transfer trust income, without transferring the trust

property.

TRANSFER OF INCOME WITHOUT TRANSFER

OF ASSET (SEC. 60)

Section

60 is applicable if the following conditions are satisfied:

1. The taxpayer owns an asset

2. The ownership of asset is not

transferred by him.

3. The income from the asset is

transferred to any person under a settlement or agreement.

If

the above conditions are satisfied, the income from the asset would be taxable

in the hands of the transferor i.e. the settlor.

10. Tax treatment in the hands of

settlor-when property is transferred by him to the trust? Transfer of capital assets – section 47(iii) of the Income

Tax Act, 1961 any transfer of a capital asset under a gift or will or an

irrevocable trust is not regarded as transfer and hence not

subjected to capital gain tax. If a person settles any property under an

irrevocable trust, then he is not required to pay any capital gain tax on such

transfer.

11. Minor and private trust-tax

consequences? INCOME OF MINOR CHILD (SEC. 64 (1A))

- All income which arises or accrues to the minor child

shall be clubbed in the income of his parent (Sec. 64(1A), whose total

income (excluding Minor’s income) is greater.

- However, in case parents are separated, the income of

minor will be included in the income of that parent who maintains the

minor child in the relevant previous year.

- Thus, in case of private trusts where minors are

beneficiaries and their parents are alive, then the income from trust

property will be clubbed in the hands of the parents as mentioned above.

12. Spouse and private trust-tax

consequences?

INCOME FROM ASSETS TRANSFERRED TO A

PERSON FOR THE BENEFIT OF SPOUSE [SEC. 64 (1) (VII)]

Income from assets transferred to a

person for the benefit of spouse attract the provisions of section 64 (1) (vii)

on clubbing of income. If:

- The taxpayer is an individual.

- He/she has transferred an asset to a person or an

association of persons.

- Asset is transferred for the benefit of spouse.

- The transfer of asset is without adequate

consideration.

In case of such individuals income

from such an asset is taxable in the hands of the taxpayer who has transferred

the asset. Thus where a person intends to transfer any property to a trust for

the benefit of his/her spouse, then the income shall be clubbed in the hands of

the transferor.

13.

Daughter-in-law (son’s wife) and private trust-tax consequences?

INCOME

FROM ASSETS TRANSFERRED TO A PERSON FOR THE BENEFIT OF SON’S WIFE [SEC. 64 (1)

(VIII)]

Income

from assets transferred to a person for the benefit of son’s wife attract the

provisions of section 64 (1) (vii) on clubbing of income. If,

- The taxpayer is an individual.

- He/she has transferred an asset

after May 31, 1973.

- The asset is transferred to any

person or an association of persons.

- The asset is transferred for

the benefit of son’s wife.

- The asset is transferred

without adequate consideration. In case of such individual, the income

from the asset is included in the income of the person who has transferred

the asset.

14.

Is private trust a real tax planning tool?

In

most of the cases people are confronted with the issue as to whether private

trust is at all a tax saving tool in the hands of the tax payer (consider the

time, money and energy spent on creating the private trust).

Is

it at all worth creating a private trust?

In

our opinion, the biggest misconception in the minds of people is that by

creating multiple private trusts for a single beneficiary, the tax can be saved

by each trust by claiming tax as per the tax slab.

Consider

the following example: Mr. X has 4 properties and he has one son “Y” of 20

years of age. He wants to create private trust for his son. He creates 4

private trusts in order to claim basic exemption

{kind=link}

- Total income from all the

properties: Rs. 6,60,000.00 Actual tax +EC for AY 12-13 (for male below

the age of 60 years) 65,920.00

- Now, Mr. X believes that by

creating for 4 trusts he can save Rs. 65,920.oo tax.

- However, it may be clearly

mentioned here the A.O. has the has the option to make the assessment

directly on the beneficiaries as per section 166.

- In our opinion, a private is

only a protection tool as against the tax planning tool. It can be used to

protect the interests of the beneficiaries, but the beneficiaries have to

pay the legitimate tax, which is otherwise payable by them in case they

were not shielded by the private trust.

15. Whether private trust can claim

deductions u/c VIA? Yes, a private trust which

invests/incurs expenditure on behalf of the beneficiary is eligible to claim

deduction u/c VIA and further is also eligible for set-off and carry-forward of

losses.

16. More FAQs

1.

Whether a settlor can have more than one private trust?

Yes,

a settlor can have more than 1 private trust. This depends on his tax planning.

2.

How immovable property is to be transferred to the private trust?

The

property is transferred by a duly registered transfer deed/trust deed. The

stamp duty is applicable. Please contact your local civil lawyer to know more

on this.

3.

Whether registration is necessary even if the settlor owns the property?

Yes,

but only in the case of property being immovable property.

4.

Whether immovable property is to be transferred in the name of only one trustee

(where more than one trustee is present in one trust)?

The

trust is a juridical artificial person and the trust property will be

transferred to the trust and the property will be managed by the trustee. The

name of the trustee (s) will appear on the deed of transfer in representative

capacity

5.

If the private trust is for a sole beneficiary (single beneficiary) but

trustees are more than 1, then who will be liable for income tax as

representative assesse?

The

person who is the managing/head trustee or any trustee authorized in this

behalf by the board of trustees

It

is advised that the readers should take proper care and consultation before

acting on the material contained in this article.

————————————————

Authored By-

1. M. K. Shah Advocate 2. CA Bhupesh

Kumar Shah

11/3, Butler Road, Dalibagh,

Lucknow- 226001

Email- bhu790@yahoo.com

Author 1 is a practicing income tax

lawyer at Lucknow-UP

Author 2 is a member of the

institute of Chartered Accountants of India

(Article was First Published on

13.10.2012)

No comments:

Post a Comment